How Beijing is running the EV playbook on humanoid robots — and why the West is already behind

Executive Summary

- China shipped 90% of the world's 13,000 humanoid robots in 2025, with Unitree (5,500 units) and AgiBot (5,168 units) each outselling Tesla's entire Optimus production target. The 2026 Spring Festival Gala — China's Super Bowl — featured synchronized kung-fu-fighting humanoids, turning industrial policy into prime-time spectacle.

- The humanoid robot market is projected to reach $38 billion by 2035 and $5 trillion by 2050 (Goldman Sachs/Morgan Stanley), making this arguably the most consequential industrial race of the century — and China is applying the same state-backed, scale-first strategy that made it the undisputed EV superpower.

- The rare earth bottleneck creates a geopolitical chokepoint: every humanoid's actuators and motors depend on NdFeB permanent magnets, and China controls 90% of rare earth processing — meaning the West's humanoid ambitions run through Beijing's supply chain.

Chapter 1: The Kung Fu Moment

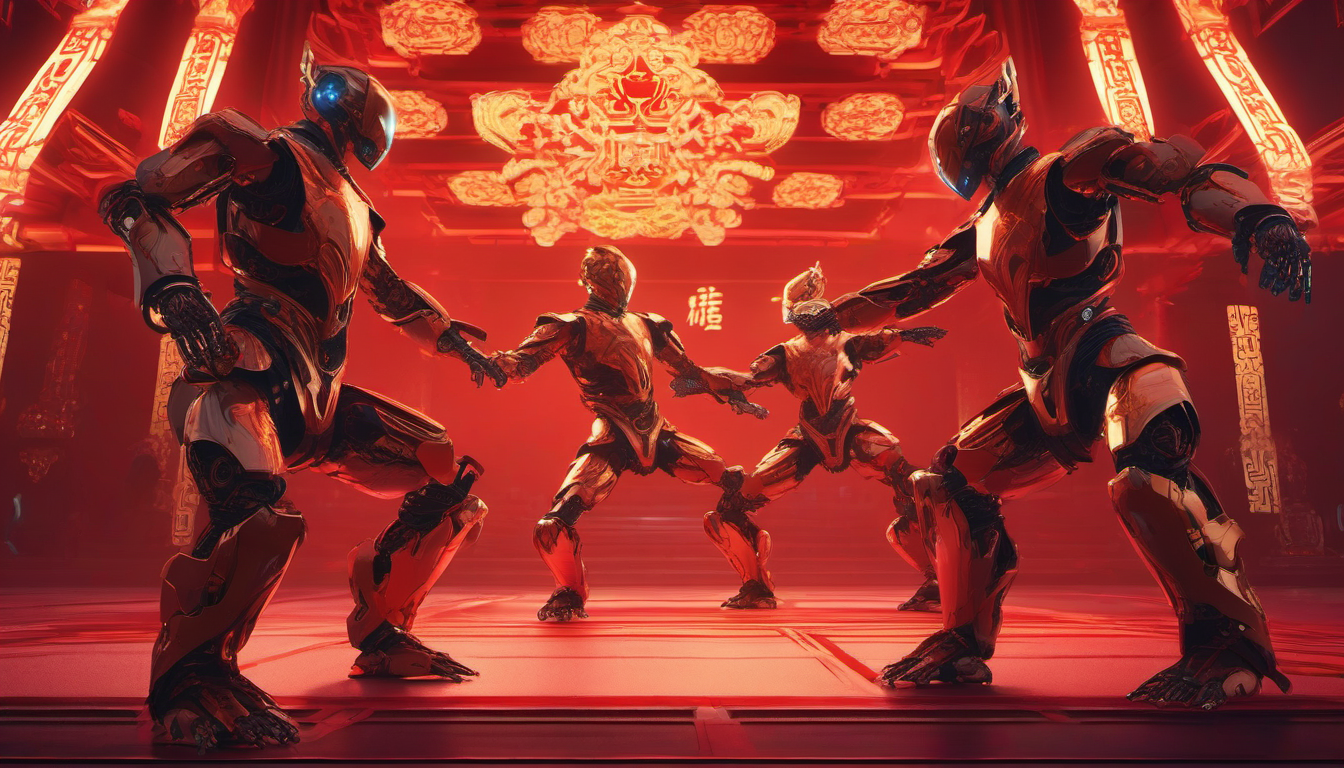

On February 16, 2026, over a dozen humanoid robots from Unitree Robotics walked onto the stage of CCTV's Spring Festival Gala — the most-watched television event on the planet, commanding 79% of China's live TV viewership the previous year. They weren't dancing or waving. They were performing synchronized martial arts: sword work, pole fighting, nunchuck sequences, and the technically demanding wobbles and backward falls of China's "drunken boxing" style, all in close proximity to child performers.

This wasn't Unitree's first gala appearance. In 2025, sixteen full-size humanoids twirled handkerchiefs alongside human dancers, a spectacle that earned Unitree's founder Wang Xingxing a meeting with President Xi Jinping at a high-profile tech symposium weeks later — the first such gathering since 2018. Xi has since met five robotics startup founders in the past year, on par with the four EV and four semiconductor entrepreneurs he met in the same period.

The message is unmistakable. As Beijing-based tech analyst Poe Zhao put it: "Humanoids bundle a lot of China's strengths into one narrative: AI capability, hardware supply chain, and manufacturing ambition. In an early market, attention becomes a resource."

Georg Stieler, Asia managing director at technology consultancy Stieler, was more direct: "Companies that appear on the gala stage receive tangible rewards in government orders, investor attention, and market access." The pipeline from industrial policy to prime-time spectacle is uniquely Chinese — and uniquely effective.

Chapter 2: The Numbers That Matter

The humanoid robot industry is still in its infancy. Between 13,000 and 18,000 units were sold globally in 2025. But the distribution tells the real story.

| Metric | China | United States |

|---|---|---|

| Global shipment share (2025) | ~90% | ~5% |

| Top company units sold | Unitree: 5,500 / AgiBot: 5,168 | Figure AI: ~150 / Agility: ~150 / Tesla: ~150 |

| Unicorns (>$1B valuation) | 13+ companies | 6 companies |

| IPOs planned (2026) | AgiBot, Unitree | None confirmed |

| Entry-level pricing | Unitree R1: $4,186 | Tesla Optimus: TBD (est. $20,000-30,000) |

| State visits from head of state | 5 robotics founders met Xi in 12 months | 0 |

The neck-and-neck race between Unitree and AgiBot mirrors how China built its EV dominance: early state support enabled dozens of entrants, rapid scaling drove costs down, and a few champions emerged to dominate global bestseller lists. BYD followed this exact trajectory from obscurity to overtaking Tesla in global sales.

Morgan Stanley projects China's humanoid shipments will more than double to 28,000 units in 2026. By 2035, Goldman Sachs estimates the global market at $38 billion. By 2050, Morgan Stanley sees $5 trillion.

Chapter 3: The EV Playbook, Reloaded

China's humanoid robot strategy is not improvised. It is a deliberate replay of the electric vehicle playbook — and the parallels are striking.

Phase 1: State designation as strategic priority. Humanoid robots were listed as a key industrial area in China's 14th Five-Year Plan in 2021, just as EVs were designated in the 13th Plan. State funding flowed to both testing infrastructure and individual companies. Provincial governments built dedicated robot training centers for workers and deployed testing environments.

Phase 2: Massive entry and price war. China now has over 800 humanoid-related companies. The price competition is already visible: Unitree's R1 companion robot retails for $4,186, while Noetix's Boomi launched at an even lower price point. This mirrors how BYD's Seagull entered at $10,000, undercutting Western competitors by 60-70%.

Phase 3: Supply chain verticalization. Chinese manufacturers increasingly use domestic components — motors, sensors, actuators, controllers — reducing costs and accelerating time-to-market. The same local supply chain that produces the world's drones, EVs, and consumer electronics is being repurposed for humanoids.

Phase 4: Automaker convergence. This is where 2026 diverges from the EV template. China's automakers — bruised by the devastating EV price war that destroyed $68 billion in value — are pivoting hard into robotics. Chery deployed a traffic-police humanoid at a Wuhu intersection in January. Seres (Huawei's EV partner) formed a robotics venture with ByteDance's Volcano Engine. XPeng is developing its own humanoid line. Tesla plans to repurpose its Fremont Model S/X production line for Optimus Gen 3, targeting 1 million units per year.

Elon Musk himself acknowledged the competitive reality at Davos in January: "China is very good at AI, very good at manufacturing, and will definitely be the toughest competition for Tesla. To the best of our knowledge, we don't see any significant competitors outside of China."

Chapter 4: The Rare Earth Chokepoint

Every humanoid robot's joints, actuators, and motors depend on neodymium-iron-boron (NdFeB) permanent magnets — the same critical materials at the heart of EV motors and wind turbines. China processes approximately 90% of the world's rare earth elements, including the heavy rare earths (terbium, dysprosium) essential for high-temperature magnet performance.

This creates a strategic paradox: the West cannot build humanoid robots at scale without materials that flow through Chinese refineries.

The recently launched CME NdPr futures contract (the world's first rare earth financial benchmark) is an attempt to break Beijing's pricing monopoly, but it addresses price transparency, not physical supply. MP Materials in California and Lynas in Australia are expanding capacity, but neither can match Chinese processing volumes before 2030.

If humanoid production scales as projected — from 13,000 units in 2025 to potentially millions by the 2030s — rare earth demand for robotics alone could rival current EV consumption. Each full-size humanoid requires dozens of high-performance servo motors, each containing NdFeB magnets. At scale, this creates a new front in the resource competition that already defines the US-China technology rivalry.

Chapter 5: Scenario Analysis

Scenario A: China Dominance (45%)

Thesis: China replicates the EV pattern — early scale advantage becomes insurmountable.

Evidence:

- In EVs, China went from 0% to 60%+ global EV production share in under a decade. The humanoid starting position (90% share) is even more dominant.

- Chinese firms have a 35:1 unit advantage over US competitors. Network effects in AI training data (more deployed robots = more real-world data = better AI) compound this lead.

- IPO capital (AgiBot, Unitree) accelerates hiring and R&D, while Western competitors remain private and capital-constrained.

Trigger: AgiBot or Unitree IPOs succeed, raising $5B+; first mass deployment in Chinese factories (1,000+ units at a single facility) demonstrates commercial viability.

Historical precedent: DJI's drone dominance — early Chinese scale, aggressive pricing, and vertical integration captured 70%+ of the global consumer drone market by 2020, a position never recaptured by Western competitors.

Scenario B: Western Catch-Up via AI Software (35%)

Thesis: Hardware is necessary but not sufficient; the real value accrues to AI software and autonomy, where the US still leads.

Evidence:

- Omdia analyst Lian Jye Su: "Western humanoid companies can compete by focusing on superior AI, software, and autonomy rather than sheer hardware volume."

- Tesla's Optimus benefits from the same neural network infrastructure powering FSD. Figure AI's partnership with OpenAI provides frontier model access.

- US regulatory environment may restrict Chinese humanoid imports on national security grounds (ITAR, CFIUS), creating a protected domestic market.

Trigger: Tesla achieves autonomous task completion rates >90% in factory settings; US imposes tariffs or bans on Chinese humanoid imports citing security concerns.

Historical precedent: Apple iPhone vs. Chinese smartphone makers — despite cheaper hardware from China, Apple maintained premium market share through software ecosystem lock-in.

Scenario C: Fragmented Coexistence (20%)

Thesis: The market bifurcates — China dominates industrial/manufacturing humanoids, the West leads in consumer/service applications.

Evidence:

- Chinese robots excel at repetitive factory tasks; Western robots may excel at unpredictable consumer environments requiring advanced reasoning.

- Geopolitical decoupling creates parallel ecosystems, similar to the current AI chip bifurcation (Nvidia vs. Huawei Ascend).

- Japan and South Korea (Hyundai/Boston Dynamics) emerge as third-force players.

Trigger: EU and US adopt "Buy Western" procurement policies for service robots; Japan deploys elder-care humanoids at scale, demonstrating a non-Chinese alternative.

Chapter 6: Investment Implications

Direct beneficiaries:

- Rare earth miners/processors: MP Materials (MP), Lynas Rare Earths (LYC.AX), and Chinese processors benefit from structural demand growth. The CME NdPr futures contract creates new hedging and speculation opportunities.

- Servo motor and actuator suppliers: Harmonic Drive Systems (6324.T), Nabtesco (6268.T), and domestic Chinese equivalents like Leaderdrive are essential component suppliers.

- AI chip makers: Nvidia's GPU demand expands beyond data centers to robotics training and inference. Humanoid deployment at scale requires edge AI chips — benefiting Qualcomm, MediaTek, and potentially Huawei's Ascend line.

Indirect beneficiaries:

- Factory automation integrators: Companies like Fanuc (6954.T) and ABB that integrate humanoids into existing production lines.

- Insurance/liability: As humanoid deployment scales, product liability and workplace safety insurance become new markets.

Risk exposures:

- Labor-intensive industries in aging societies: Japan, South Korea, and Germany face the highest potential disruption — but also the highest adoption incentive.

- Traditional industrial robotics: KUKA, Yaskawa, and conventional robot arm manufacturers face potential commoditization if humanoids prove versatile enough to replace fixed automation.

| Asset Class | Short-term (2026) | Medium-term (2028-2030) | Long-term (2035+) |

|---|---|---|---|

| Chinese robotics stocks | High volatility, IPO-driven | Scale-up winners emerge | Potential $100B+ market caps |

| Rare earths | Steady demand growth | Acute shortage risk | Strategic commodity |

| AI chips (Nvidia et al.) | Incremental demand | Meaningful revenue line | Transformative |

| Traditional auto (non-pivot) | Margin pressure | Existential threat | Adapt or decline |

Conclusion

The 2026 Spring Festival Gala moment — robots performing kung fu on the world's most-watched stage — is not just spectacle. It is the visible tip of a $5 trillion industrial strategy that China has been executing with the same systematic precision it brought to EVs, solar panels, and batteries.

The West is not without advantages. American AI software, Tesla's neural network infrastructure, and Japan's precision manufacturing heritage all represent genuine capabilities. But capabilities are not the same as deployed scale, and in hardware-intensive industries, scale tends to win.

The critical question is not whether humanoid robots will transform manufacturing, eldercare, logistics, and services — Morgan Stanley and Goldman Sachs have already priced in that transformation. The question is who will build them, who will control the supply chain, and who will capture the value.

Right now, 90% of the answer is Chinese. Whether the remaining 10% can grow before the window closes will define the next decade of the AI-robotics industrial revolution.

Sources: Reuters, Rest of World, Bloomberg, CNBC, Omdia, Morgan Stanley, Goldman Sachs, Tech Startups

Leave a Reply